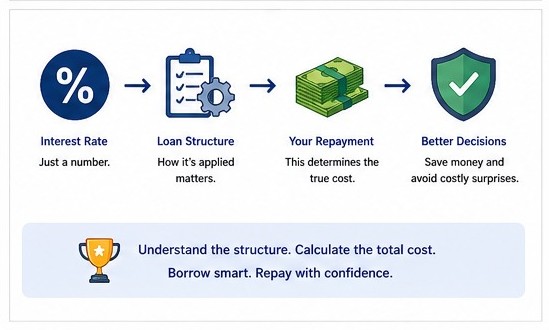

Learn how interest rates really affect your loan repayment and how to calculate the true cost of a loan.

Most people glance at a loan’s interest rate and assume they understand the cost. But the truth is, the percentage alone can be quite misleading. What really matters is how the interest rate on a loan is applied, and the way interest is calculated directly affects your total loan repayment and the cost of borrowing.

One of the leading causes of loan default is failure to understand how the interest rate and the loan work, because such borrowers later find out that the loan has become an expensive burden.

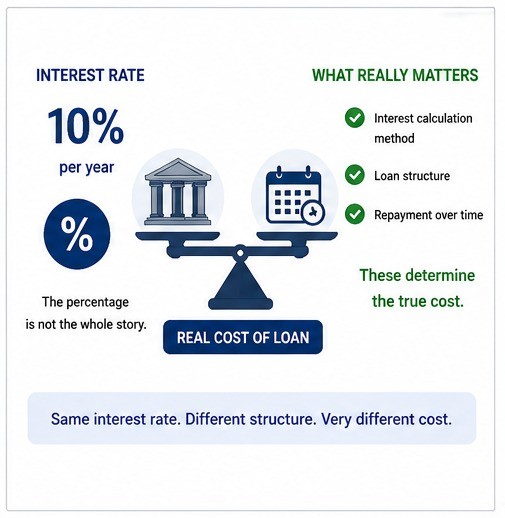

An interest rate is the cost of borrowing money, expressed as a percentage of the amount taken. Normally, it seems straightforward, just a number that tells you how much extra you will pay on top of what you borrowed. But that number, by itself, is incomplete. What really determines the total cost of a loan is not just the percentage, but how that percentage is applied over time.

This is where many borrowers get misled. Two loans can be of the same interest rate, say 10%, yet end up costing very different amounts depending on how the interest is calculated and charged.

Most people understand the basic idea that higher interest means paying more. What’s less obvious, and far more important, is the structure behind that loan interest rate and how it affects your loan repayment over time.

Consider a simple but often overlooked example. Suppose you borrow 1,000,000 at an interest rate of 10% per year for 10 years. At a glance, that might sound like a manageable loan. However, if the interest calculation method uses a flat or simple approach, in which 10% is charged each year on the original amount, the numbers tell a very different story.

Each year, you would pay 100,000 in interest. Over 10 years, that adds up to 1,000,000 in interest alone. When you include the original amount borrowed, your total loan repayment becomes 2,000,000. In other words, you end up paying back double what you borrowed, even though the interest rate never changed and remained at “just 10%.”

This is not a trick or an error. It is simply a different way of applying loan interest. And unless you are paying close attention to how the interest rate is applied, it is easy to miss.

To understand, let’s distinguish between two common ways interest rates on loans are applied.

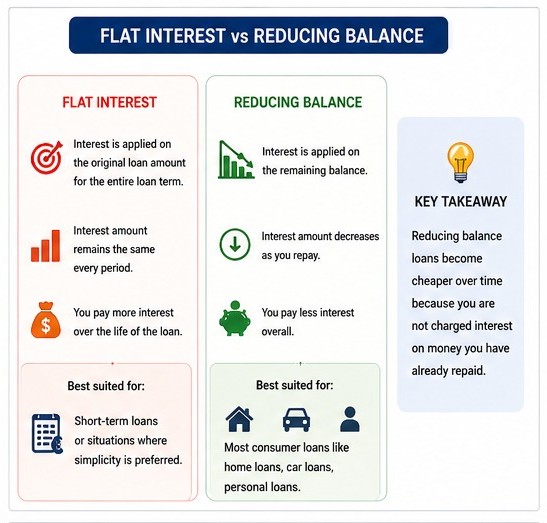

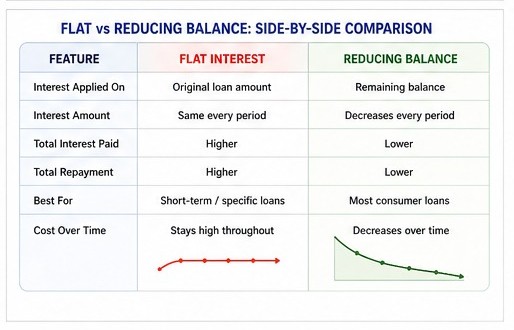

With flat interest, the interest rate is applied to the original loan amount for the entire duration of the loan. It does not matter how much of the loan you have already repaid; the loan interest is always calculated on the full principal. This keeps the interest portion constant and often leads to a higher total cost of a loan over time.

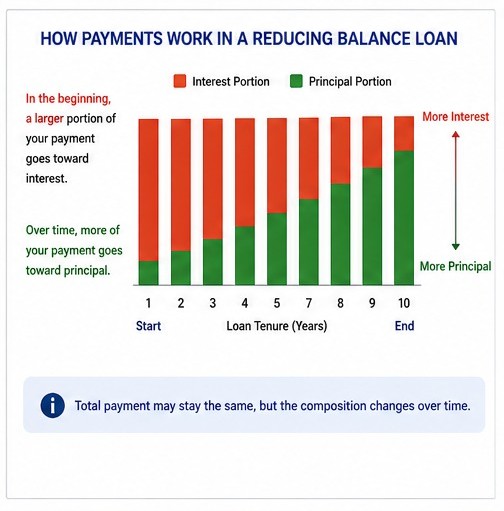

In contrast, most standard consumer loans, such as car loans, mortgages, and many personal loans, use a reducing balance method. In this structure, the interest rate on the loan is applied to the remaining balance. As you make payments and the balance decreases, the interest charged also declines.

This difference may seem technical, but it has a significant financial impact on your loan repayment. A reducing balance loan naturally becomes cheaper over time because you are no longer being charged interest on money you have already repaid.

In real-world borrowing, the distinction between these interest calculation methods is not always clearly explained. Loan offers tend to highlight the interest rate while leaving the actual loan interest calculation in the fine print.

This is particularly relevant in certain types of lending. Some business loans, informal lending arrangements, and short-term or quick-access loans may use flat-style calculations or include fixed charges that effectively behave like flat interest. The advertised interest rate on a loan may appear reasonable, but the actual total repayment can be much higher than expected.

Meanwhile, even in reducing balance loans, the timing of payments and the way interest is applied can influence how much you pay overall. Interest may be calculated monthly, and in the early stages of loan repayment, a larger portion of each payment goes toward interest rather than reducing the principal. Over time, that balance shifts, but the early cost can still be substantial.

All of this reinforces a key point, which is that the interest rate alone does not define the total cost of a loan. The structure behind the loan interest rate does.

Rather than focusing only on the interest rate, a more reliable approach is to look at the total loan repayment amount. This is the clearest measure of what the loan will actually cost you.

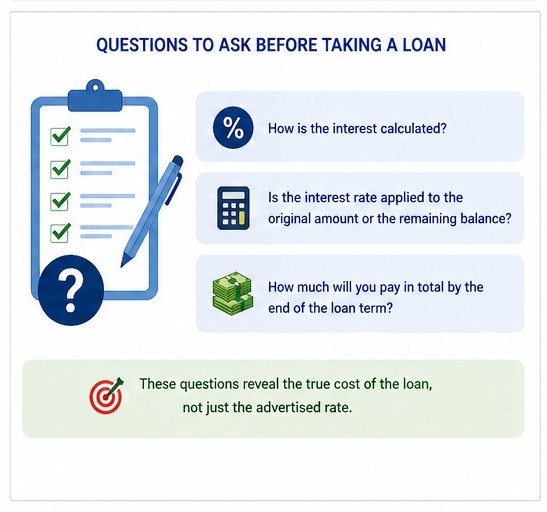

Before agreeing to any loan, it is worth asking a few direct questions:

* How is the interest calculated?

* Is the interest rate applied to the original amount or the remaining balance?

* How much will you pay in total by the end of the loan term?

These questions cut through the surface-level presentation and reveal the real financial commitment. They also make it easier to compare different loans based on their true cost of borrowing, not just the advertised interest rate.

In practice, what matters is not how attractive the rate sounds, but how much money ultimately leaves your pocket for loan repayment.

Interest rates are often presented as simple percentages, but they operate within structures that can significantly affect your loan repayment. A loan that appears affordable at first can become expensive depending on how the interest rate is applied, while a slightly higher rate under a more favorable structure may actually result in a lower total cost of the loan.

Understanding this distinction is not about mastering complex financial theory. It is about recognizing that the headline interest rate is only part of the story. The real cost of borrowing lies in the details, in how loan interest is calculated, when it is applied, and how it interacts with your repayments over time.

Once you begin to look at loans this way, they become easier to evaluate and harder to misinterpret. And that awareness alone can help you avoid decisions that might otherwise seem reasonable at first, but prove costly later on.